Mobiles pass PCs as biggest systems market and IC user

Total worldwide production value of electronic systems is projected to increase 4% in 2013 to $1.41 trillion and climb to about $1.74 trillion in 2017, which represents a compound annual growth rate (CAGR) of 5% from $1.36 billion in 2012, according to IC Insights’ 2014 edition of ‘IC Market Drivers - A Study of Emerging and Major End-Use Applications Fueling Demand for Integrated Circuits’. The report examines the largest existing system opportunities for ICs and evaluates the potential for new applications that are expected to help fuel the market for ICs.

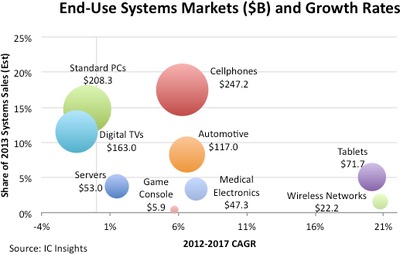

Figure 1 compares the relative market sizes and projected growth rates of nine major systems segments among the several end-use electronic product categories covered in the report. These nine market categories represented an estimated two-thirds of the total production value of all electronic systems in 2013. Mobile phones will overtake standard personal computers (desktop and notebook PCs) as the largest electronic systems market for the first time in 2013. They are expected to account for 18% of worldwide electronic systems sales ($247.2 billion) versus standard PCs with 15% ($208.3 billion) of the total in 2013.

In 2012, PCs represented 17% of systems sales while mobiles were about 16% of the total, based on the report’s market analysis. Mobile sales are projected to rise by a CAGR of 6.3% in the 2012-2017 period, while standard PC revenues are expected to slump by an annual rate of -0.7%, partly due to the growing popularity of tablet computers and greater use of smartphones to access the internet.

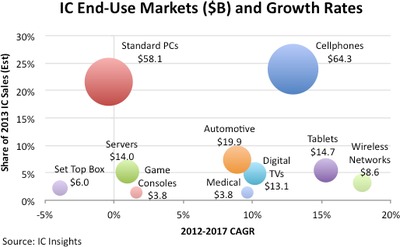

Figure 2 shows the market sizes and projected growth rates of IC sales for 10 major end-use systems categories, based on data and five-year forecasts in the report. After dominating IC sales for most of the last two decades, standard PCs will take a back seat to mobiles, which are projected to become the largest application for ICs in 2013. The report estimates mobiles will account for 24% of IC sales in 2013 versus 22% in 2012, while PCs will represent 22% of the total in 2013 compared to 25% last year. IC sales for standard PCs have stalled out while mobile IC revenues are projected to grow by a CAGR of 12.9% between 2012 and 2017.

Among these 10 end-use market segments, IC sales growth is expected to be the strongest in systems for wireless networks (a CAGR of 17.9%) and tablet computers (a CAGR of 15.3%) in the five-year forecast period of the report. IC revenues generated by these 10 end-use systems categories will represent an estimated 77% of total integrated circuit sales worldwide in 2013.

The report examines and evaluates key existing and emerging end-use applications that will support and propel the IC industry through 2017. Among the key applications covered in the report are automotive electronics, mobile phones and smartphones, personal and mobile computing, servers and cloud computing, wireless networks, digital television and video game consoles, the smart grid and smart appliances, medical/health electronics, and a review of many near- and long-term applications to watch such as autonomous vehicles, home robotics and the Internet of Things (IoT) that may provide significant opportunity for IC suppliers later this decade.

For more information, visit http://www.icinsights.com/services/ic-market-drivers/.

Australia's largest electronics expo returns to Sydney

Electronex, the annual electronics design and assembly expo, will return to Sydney on 19–20...

The fundamentals of Australian RCM compliance

The following information aims to help readers understand the Australian compliance requirements...

Largest ever Electronex Expo in Melbourne

The Electronics Design and Assembly Expo will return to Melbourne from 10–11 May at the...

")